Detailed Comparison of ISOs vs NSOs

Whether you’re receiving Incentive Stock Options (ISOs) or Nonqualified Stock Options (NSOs), you’ll want to understand their differences and similarities so you have a better idea of how to make the most of them. The purpose of this article is to give you a detailed comparison between ISOs and NSOs so you can feel more confident in making decisions with the ISOs or NSOs you’ve been granted.

Differences Between ISOs vs NSOs

There are five major differences between ISOs and NSOs. Some of these differences will have greater impact than others. Still, we think it’s important that you are aware of all the major differences - even those that may not have a huge impact on you. The following list is ranked in order from the least impactful to the most impactful.

ISO vs NSO Difference #1 - Who’s Eligible to Receive the Grant

The first difference between ISOs and NSOs is who is able to receive them. ISOs can only be granted to employees. NSOs can be granted to employees and consultants to the company.

Since ISOs in some cases are considered to be better than NSOs (which we’ll address later), they are reserved specifically for employees of the company.

Because consultants to the company can receive NSOs, it’s very common for consultants to request NSOs in addition to other fees they will be paid by the company.

ISO vs NSO Difference #2 - Limits on How Much Can Be Granted

ISOs have a limit. NSOs do not.

Since ISOs qualify for potentially better tax treatment, the IRS limits how many ISOs a company can grant to an employee.

ISOs grants are limited to $100k of exercisable value per year based on the value at grant. Anything over that amount for a given year will automatically convert to NSOs.

Here’s an example:

Say you received a grant of 40k ISOs with an exercise price of $10. The grant agreement states that 25% of the 40k options will vest each year.

The total value of this grant over 4 years is $400k ($10 x 40k ISOs), but only $100k of value is exercisable each year so this grant won’t trigger a conversion to NSOs. The following table shows what this would look like:

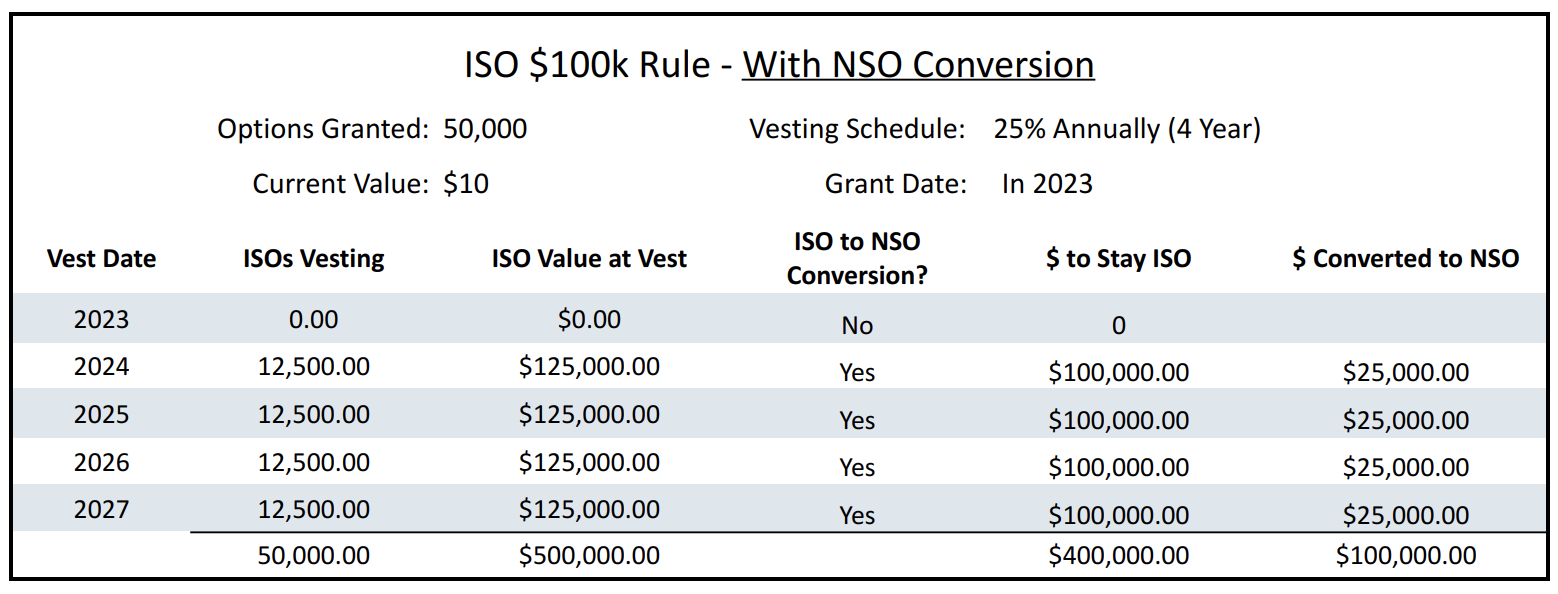

Now say you were granted 50k of ISOs over 4 years instead of 40k. This would cause you to receive $125k worth of exercisable ISO value per year, which is not allowed.

So rather than having 12,500 ISOs vest each year, you’d be eligible to receive 10k ISOs and 2,500 NSOs. Here’s what that would look like:

This $100k rule is tracked closely by your company’s equity compensation team so it’s not something you’ll need to worry about too much, but it is a major difference between ISOs and NSOs.

ISO vs NSO Difference #3 - Stage of the Company Granting the Equity

The types of equity that companies grant will vary based on how large the company is.

If a company is just starting out, it’s much more likely to offer ISOs. Companies will typically offer ISOs until the company begins preparations to go public.

After a company has gone public, ISO grants are less common and employees are much more likely to receive Restricted Stock Units (RSUs) and NSOs instead.

ISO vs NSO Difference #4 - Effects of Quitting Your Job

When you quit working for a company, you’ll want to be sure that you aren’t leaving any equity on the table. Each grant of ISO and NSO has an expiration date and sometimes that expiration date will accelerate when you quit. So before you quit or as you’re quitting, be sure you understand your company’s policies regarding vested ISOs and NSOs.

In addition to a potential acceleration of the expiration date, your options may change types after quitting.

NSOs will stay NSOs, so that’s easy to remember.

But ISOs, on the other hand, will convert to NSOs 90 days after your last day at work (and sometimes even sooner). Having ISOs convert to NSOs isn’t the end of the world, but it’s certainly something you should be aware of and plan for.

ISO vs NSO Difference #5 - Taxation

This is the biggest difference between ISOs and NSOs.

ISOs have the option for preferential tax treatment. NSOs do not.

When you exercise ISOs, the difference between the current market price and the exercise price doesn’t create ordinary income. (It does create an Alternative Minimum Tax adjustment, but that likely won’t cause you any tax liability unless your spread on the ISOs is large.)

If you hold onto your ISOs for two years from the grant date and one year from the exercise date, everything will be treated as long term capital gains when you sell. This means that your max tax rate will be 20%.

When you exercise NSOs, the difference between the current market price and the exercise price will be immediately taxable at your ordinary income tax rates. And those rates can be as high as 37%. The immediate tax burden of NSOs typically means that you’ll want to sell a portion of your options to ensure you have funds to cover the taxes.

Similarities Between ISOs vs NSOs

Understanding the similarities between ISOs and NSOs will help you realize that, in some cases, there’s not much difference between the two.

ISO vs NSO Similarity #1 - Terminology is Identical

Once you get used to equity compensation lingo, it’s pretty much all the same terminology.

Grant date, exercise price, exercise date, fair market value, and spread are all common terms that you should be familiar with. If you’re unfamiliar with this terminology, we recommend that you review our Glossary and read our 11 Terms to Know If You Have Nonqualified Stock Options articles for explanations of these often-used terms.

ISO vs NSO Similarity #2 - Taxes on Gains from Exercise On

Any gain above from the date of exercise will follow the same rules. Whether you have ISOs or NSOs, the gains from the exercise date on will either be short term capital gains or long term capital gains.

Here’s a comparison of the two to help put it together:

ISO vs NSO Similarity #3 - Ability to Grow with Your Company

The single best part of receiving ISOs and NSOs is that they give you a remarkable opportunity to grow with your company.

If you receive options while a company is still in its hyper-growth years, you’ll be very happy down the road when you can exercise and sell them for a big chunk of change (even if a sizable piece of that chunk will have to go to the IRS).

ISO vs NSO Similarity #4 - You Have Control Over the Timing

One of the biggest perks of ISOs and NSOs over RSUs is that you can control the timing of taxes.

You choose when to exercise, how much to exercise, and when to sell.

This control may not seem like a big deal, but the ability to exercise or to sell over several years can save you lots of money by keeping you in lower tax brackets or in the case of ISOs, avoiding Alternative Minimum Tax (AMT).

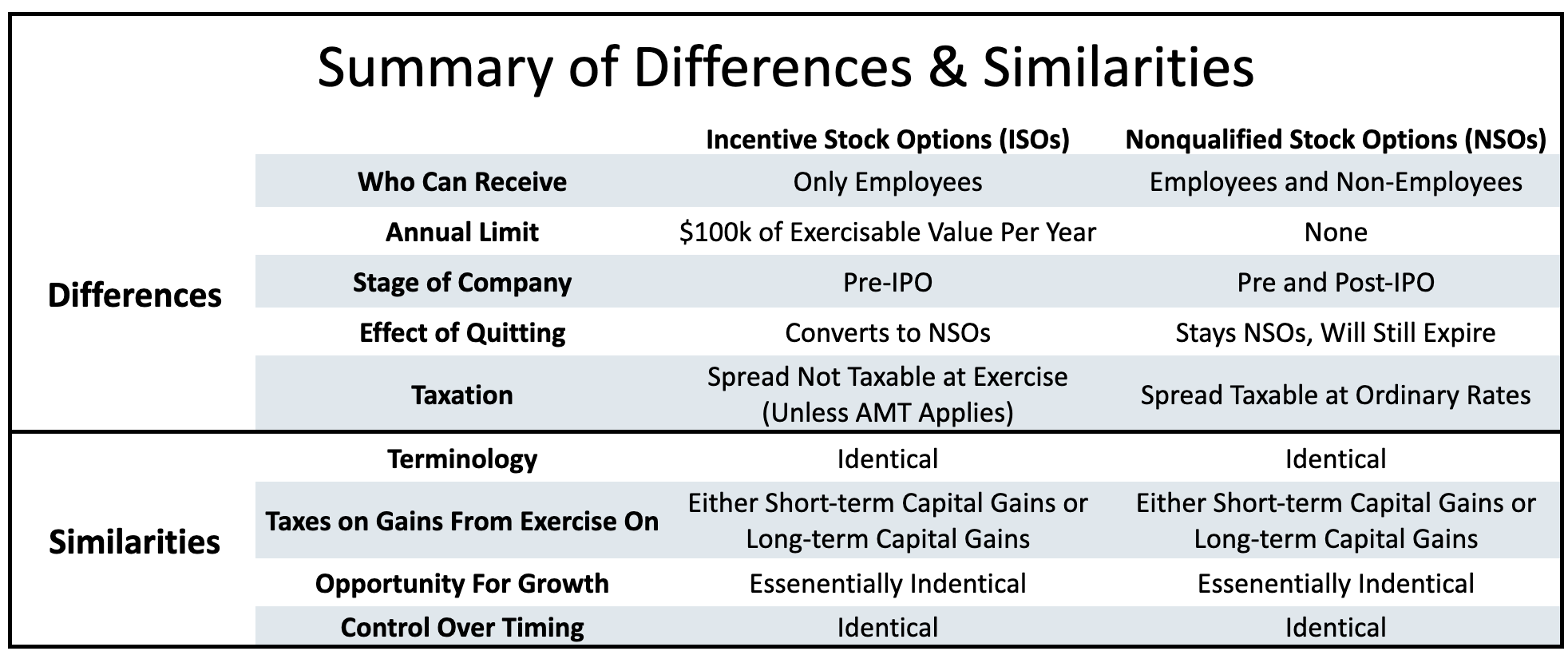

Summary of ISOs vs NSOs Differences & Similarities

We’ve reviewed a lot of differences and similarities between ISOs and NSOs so we wanted to summarize them here.

This summary isn’t meant to be an exhaustive list, but it’s a great intro list of the major differences and similarities.

Tips for Managing ISOs and NSOs

Our general recommendation is that if you feel confident in your company’s future, you should exercise options as soon as you can - with a big caveat that you shouldn’t put in more money than you’re willing to lose.

Exercising early will save you a lot of taxes down the road.

If you missed your chance to exercise early and exercising is going to cause you to take a tax hit, we recommend talking with a CPA or CFP with expertise in ISO and NSO tax strategy. It is likely that you’ll want to exercise and sell a portion of your holdings to ensure that you can cover the taxes.

We’ve seen too many cases where people owe significant taxes from exercising but, for whatever reason, don’t sell any shares. Sure enough, when the share price decreases, they are left owing more taxes than their shares are now worth. Exercising ISOs and NSOs with large spreads is not something to take lightly.

We plan to write articles providing examples of equity compensation pitfalls and how to avoid them, as well as articles addressing the different exercise strategies that work best to manage each type of equity. Once they’re written, we’ll provide the links here.

As always, please feel free to reach out to us if you have any questions regarding your ISOs or NSOs. We’re happy to help and/or refer you to a financial expert who can.