Nonqualified Stock Option (NSO) Tax Treatment & Scenarios

If you’re receiving Nonqualified Stock Options (NSOs), you’ll want to understand how NSOs are taxed. Tax treatment of different equity types varies significantly, so rather than covering multiple equity types at once, this article will only discuss how NSOs are taxed.

In this article, we’ll start by covering the basic tax treatment of NSOs, then go over tax-related things to watch out for with NSOs, and then we’ll go through some examples to help everything connect and make sense. We’ll then finish with some final thoughts and recommendations.

Basic Tax Treatment of Nonqualified Stock Options (NSOs)

Nonqualified Stock Options (NSOs) tax treatment isn’t too terribly complex once you become familiar with the different terms associated with them. We’ve covered the basic terms in this article so you can do a quick review.

You can owe taxes due to your NSOs on two different occasions:

Occasion #1 - When you exercise your NSOs

Occasion #2 - When you sell the shares you received from exercising your NSOs

Every company is different, but even if your company is public (traded on the stock market) or private (not traded on the stock market), you will still likely owe taxes on these two occasions. We’ll get into the exceptions in a bit.

Let’s take a look at each tax occasion.

NSO Tax Occasion #1 - At Exercise

When you exercise an NSO, you pay the company who issued the NSO the exercise price (also known as the strike price) to buy a share of company stock.

If the exercise price is $10 and you have 100 NSOs, you would pay the company $1,000 to exercise your 100 NSOs and the company would give you shares of stock. Even if the company’s price per share is currently worth more than $10, the company is allowing you to purchase shares at a discount. A pretty sweet deal!

The downside to having an embedded gain at the time of exercise is that when you exercise, there’s a tax calculation that’s made.

Following the example above, if you were to exercise an NSO for $10, but the company price per share is actually $20, you’d be locking in a gain of $10 per option you exercise. This is known as the bargain element or spread.

For NSOs, the IRS treats this bargain element/spread as income to you, even though all you’ve received are shares of the company. So depending on your tax rate and how many NSOs you exercised, this could put you on the hook for a pretty large sum in taxes.

The company that issued you the NSOs will likely withhold taxes for you if you still work there. But, if you’re no longer employed by the company that issued you the NSOs, the company may require some form of withholding at exercise. If they don’t, then you’ll need to make sure that you’re taking your exercised NSOs into account when it’s tax time.

NSO Tax Occasion #2 - When You Sell

The second occasion in which you’ll likely owe taxes on your NSOs is when you sell the shares you received from exercising your NSOs.

After you’ve exercised, any gain you lock in from selling the shares will be treated as a short term capital gain or long term capital gain.

Short term capital gains treatment is given when you hold an investment for less than one year and sell.

Long term capital gains treatment is given when you hold an investment for longer than one year.

The reason you hear so much about long term capital gains in the news is because the rate on long term capital gains caps out about 15-17% less than the rate on short term capital gains or ordinary income tax rates. It’s also a hot topic and may go away for people earning more than $1m in a given year.

After exercising your NSOs, if the stock price drops and you sell, you’ll be able to take a loss and put it toward other gains you’ve had in the year. If the price drops dramatically or you lose everything after exercise, you’ll be able to carry those losses forward to future years in which you have gains from other investments.

NSO Tax Treatment - Things to Watch Out For

There are three major things to watch out for if you’ve received a grant of NSOs and are planning on exercising them.

#1 - Ensure you have enough funds to cover the taxes owed from exercising your NSOs

After exercising NSOs, you’ll want to make sure you have a plan to gather the cash you’ll need to pay the taxes you’ll now owe. You can do this by selling your NSOs immediately or shortly after exercise. If your company is still private, then you’ll need to find some other way to cover the tax bill.

Regardless of how you do it, you’ll want to make sure you’ve set aside cash. The last thing you’d want to do is have to take out a loan to pay for the taxes.

#2 - Hesitancy to sell after exercising your NSOs

We see this one frequently. If you’ve exercised NSOs, you may find it hard to part ways with the shares you just acquired. The issue with waiting to sell is this: It’s very common for the share price to drop after exercise and if you need to sell shares to cover the tax bill, this means that you’ll owe taxes on a larger share value amount but will be forced to sell shares at the lower share price to cover those taxes.

So if you’re going to owe significant taxes from NSOs, the safest bet is to exercise and sell to cover your taxes. You don’t have to sell everything, but you will at least want to sell enough to cover the taxes without hesitating too long.

#3 - Not exercising early and filing an 83(b) election

Younger companies that haven’t gone public often let you exercise NSOs before they have vested. This is called early exercising.

Let’s say you were just granted NSOs at a company whose latest valuation was $8 a share. If they allow employees to early exercise before their NSOs are vested, this means that you can exercise your options so close to the grant date that the current market value might equal the exercise price.

After early exercising, there’s a form the IRS will require you to send them. This form is called an 83(b) election. In order to complete your early exercise, you must fill out this form and send it to the IRS within 30 days of your exercise.

In this $8/share example, if $8 is the current market price and $8 is the exercise price, you could exercise all of your options without incurring ANY taxes. Assuming you submitted your 83(b) election, this ensures that if the company goes up in value over the next few years, your gains when you sell would be treated as long term capital gains!

Not exercising early and filing an 83(b) election is a mistake we see often. Employees who make this mistake can end up owing significant taxes down the road. If you believe in the company you work for, it probably makes sense to early exercise.

Nonqualified Stock Option (NSO) Tax Examples

To help you figure out how to calculate the taxes you might owe from exercising NSOs or selling stock after exercising an NSO, we’ve put together three NSO Tax Examples to help you figure out which category you’d likely fall into.

For each NSO example, we’ll look at the two tax occasions mentioned earlier in this article: The Exercise Date and the Sell Date.

Note: For all of these examples, we’re going to assume that (1) all the options are 100% vested, (2) that the exercise price is $5, and (3) that the holding period after exercise is 1 year.

NSO Tax Example #1 - Flat Then Up

This first NSO tax example looks at what you’ll owe per option if the company’s stock price were to stay flat until exercise and then immediately following the exercise, the stock price were to go up.

Taxes Due at Exercise

Since the stock price started at $5 and stayed at $5 until exercise, there would be no taxes owed on the exercise date. The only thing that would need to be paid is the cost to exercise.

Taxes Due at the Sell Date

As the graph shows, on the sell date the price has risen by $10 a share since exercise. This would leave you with a $10 capital gain per share you sell.

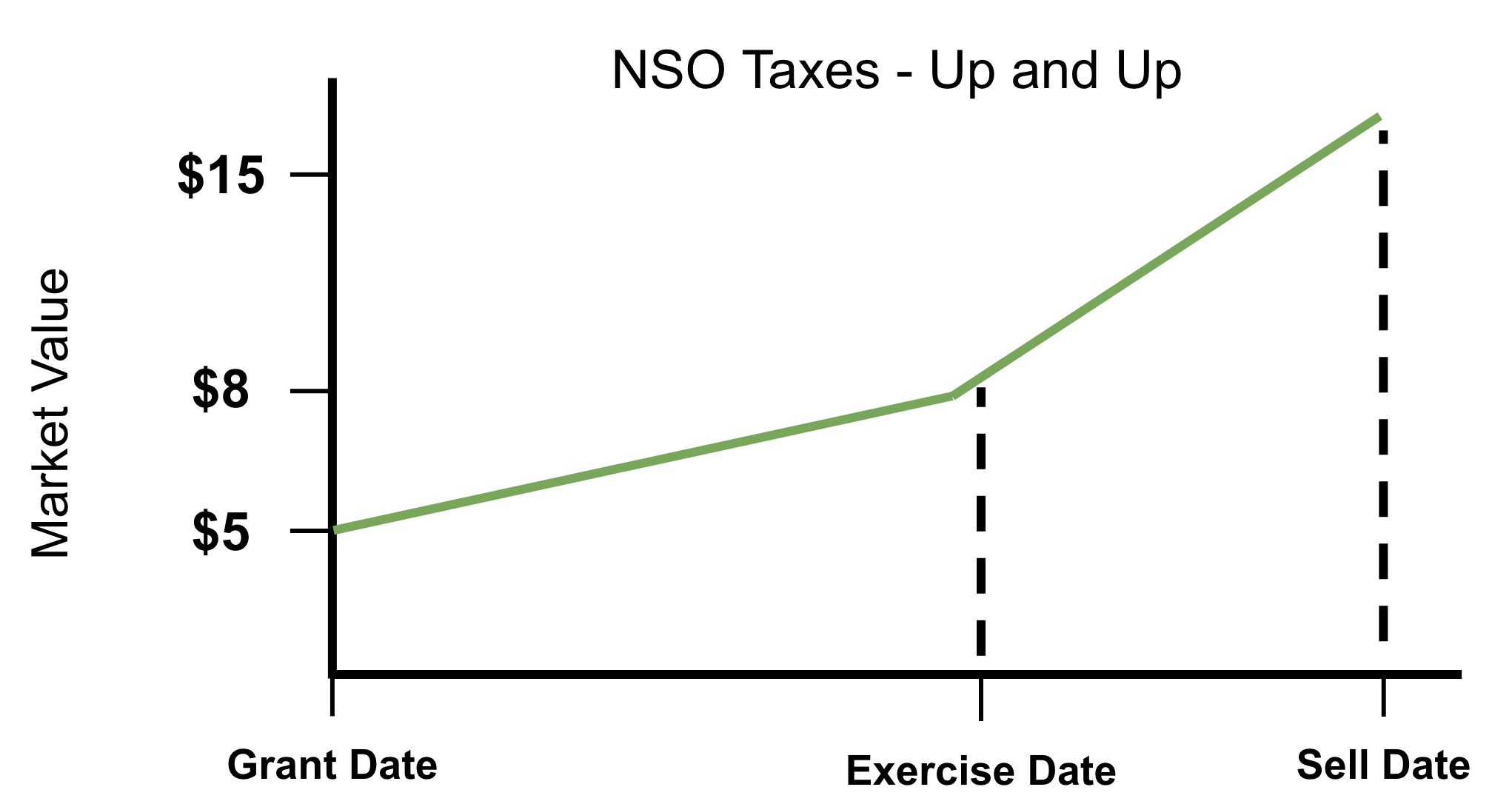

NSO Tax Example #2 - Up Then Up

This second NSO tax example is a very common scenario. The stock market is typically going up, so it’s common to see your NSOs increase in value after grant and then even more after exercise.

Taxes Due at Exercise

Since the stock price starts at $5 on the date of grant and then rises to $8 a share at the time of exercise, there’s an embedded gain of $3 per NSO. This means that for each option you exercise, you would recognize $3 of ordinary income, and you’d owe taxes on that income even if you don’t sell anything.

Taxes Due at the Sell Date

On the sell date, the price has risen by $7 a share since exercise. This would leave you with a $7 capital gain per share that you sell.

NSO Tax Example #3 - Up Then Down

After the NSO tax example #2, this is probably the next most common scenario we see play out. We’ll get into the dangers of this scenario soon, but it’s certainly the most dangerous position to be in if you’re holding on to NSOs.

Taxes Due at Exercise

Similar to the last scenario, the stock price rises from $5 to $8 at the time of exercise. This would cause $3 in additional ordinary income per NSO you exercise. Since you’d now owe taxes on that ordinary income, hopefully you’d have the cash ready.

Taxes Due at the Sell Date

On the sell date, the price has decreased by $3 a share since exercise. Since you owe/owed taxes when you exercised at $8 a share, your cost basis would equal that $8 share. Given that the stock price has dropped by $3 a share, you’d record a loss of $3 if you were to sell.

Special Consideration

This scenario doesn’t fully reflect the scale of the increases and decreases in value that can happen in real life. If you need to sell exercised NSOs to cover your tax bill, you should do it immediately. Otherwise, you run the risk of the stock price going down after exercise and being unable to afford to pay your tax liability.

NSO Tax Example #4 - Down Then Down

This scenario certainly happens, but it’s less common than you’d think. The reality is that if you hold options in a company that’s done nothing but go down, there’s a good shot that you’ll be able to negotiate with the company and ask for a refreshed grant of NSOs.

As you can see in the graph, the stock price drops before the exercise date. Remember, the exercise price of your options is $5 per NSO. So if the current price is $4, you’d lose money per option you exercise since you’d be paying $5 for something worth $4.

If this happens, you’d be better off buying the company stock directly from the stock market and letting your options stay where they are. The sell date in this example would never happen because this NSO would never be exercised.

Nonqualified Stock Options Tax Recommendations

Nonqualified stock options have a pretty straightforward tax calculation, but we’ve built out a simple NSO tax calculator for you to use anyway.

Since the spread on an NSO is treated as ordinary income when you exercise, it makes a lot of sense to sell immediately to ensure that you’ll have at least the funds you need to pay the taxes. There are plenty of cases where people who choose not to sell at exercise and end up needing to take out loans in order to pay their tax bills.

Another recommendation we have is that if you have the ability to exercise early, we generally think it’s worth considering. The biggest factor here though is that you won’t want to put in more than you’re willing to lose.

Understanding and evaluating strategies to manage your NSOs can be intimidating, especially if you hold several hundred thousand dollars worth in options. We highly recommend working with a professional who specializes in NSOs. If you need a referral, we can provide recommendations. Please feel free to reach out to us.