When Do I Owe Taxes on RSUs? (A Clear Guide)

If you work at a public company, there’s a 98% chance you’re receiving Restricted Stock Units (RSUs). They’re one of the most common forms of equity compensation, yet many employees don’t fully understand when they’ll owe taxes on their RSUs—leading to unexpected tax bills.

RSU taxation can be confusing, and because of withholding rules, you might end up owing more than you would otherwise expect come tax time.

This guide will answer the question: “When do I owe taxes on my RSUs?” and help you plan ahead so you’re not caught off guard.

By the end, you’ll know when RSUs are taxed, how to estimate what you owe, and will learn about tools to help you manage your RSUs effectively.

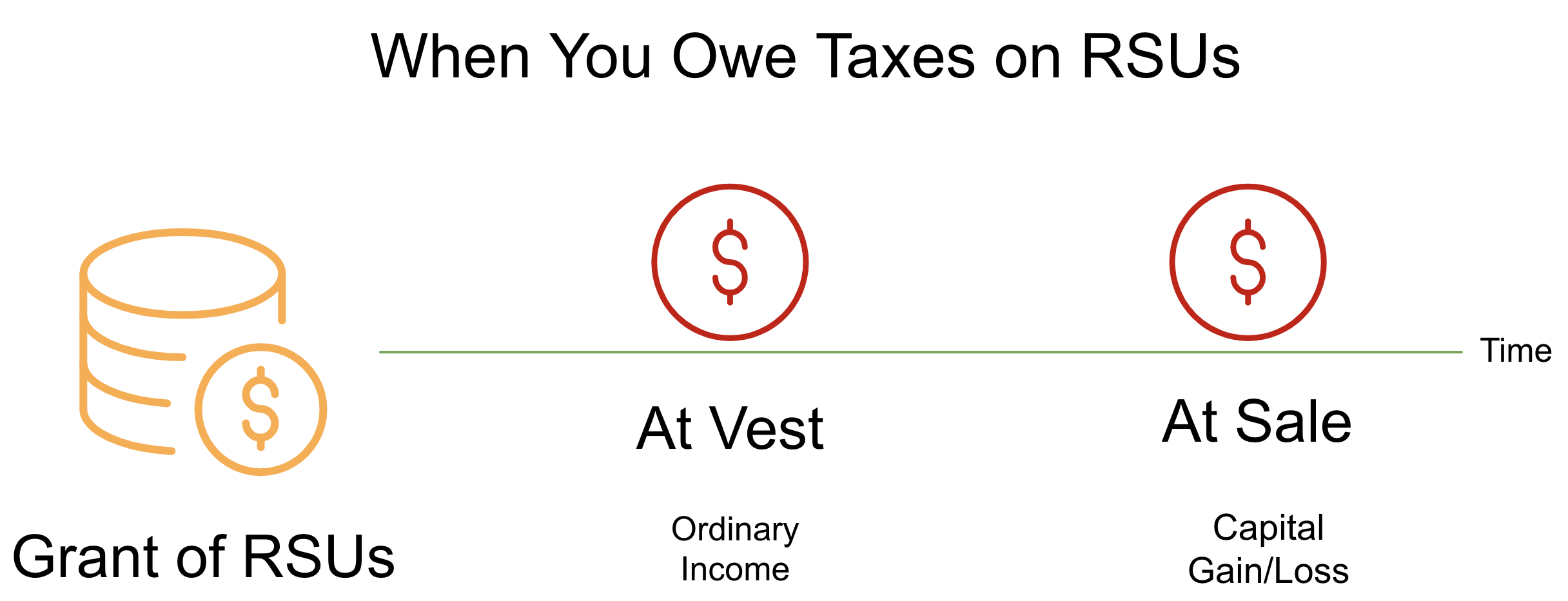

When Do I Owe Taxes on RSUs? (Short Answer)

You’ll owe taxes on the day your RSUs vest

If you sell your vested RSUs for a gain, you’ll owe additional taxes on any profit.

While this sounds straightforward, making sure enough tax is withheld can be challenging. Especially since employers often under-withhold. (More on that in a bit.)

To help you estimate whether you're at risk of owing more, we built an RSU tax calculator.

RSU Taxes at Vesting: What You’ll Owe

Few people understand all the various taxes that come into play when you receive a paycheck or when an RSU vests.

Here’s a breakdown of the four types of taxes you’ll owe when your RSUs vest:

Federal Income Tax – Varies based on your total taxable income.

Social Security Tax – 6.2% on income up to $176,100, then 0% on anything above that.

Medicare Tax – 1.45% on all wages, plus an extra 0.9% if you earn more than $200K (single) or $250K (married).

State Income Tax – Only applies in certain states like California and varies based on income.

Example: How Taxes Work on Your Paycheck

To understand how RSU taxation works, let’s first look at how a $240k salary has money withheld (no RSUs yet).

Gross Monthly Income = $20,000

Federal Tax Withholding (35%) = $7,000

Social Security Tax (6.2%) = $907 (Only applies to the first $176,100 of earnings)

Medicare Tax (1.45%) = $290

Additional Medicare Tax (0.9%) = $36 (Since earnings exceed $200K)

California Tax Withholding (10.23%) = $2,046

Take-Home Pay = $9,721

Your employer automatically withholds taxes and pays certain taxes from every paycheck so you’re covered when tax season rolls around.

If you’ve ever received a tax refund, it’s because you set aside more money throughout the year than you owed in taxes for that year.

If you’ve had to pay taxes after doing your tax return, it was because you didn’t set aside enough money throughout the year to cover the taxes you accrued (and this isn’t necessarily a bad thing).

How RSU Tax Withholdings Works

When your RSUs vest, they’re treated as income, just like your salary. This means your company withholds taxes similar to how they do it on your paycheck.

But there’s one big difference. Most companies only withhold a flat 22% for federal taxes on your RSUs, even if your actual tax rate is higher. If you have over $1 million in RSU income, the withholding jumps to 37%, but until then, companies typically withhold at 22% since that’s a government-defined statutory rate.

This means you should be aware of two things:

If you’re in a tax bracket higher than 22%, you’ll likely owe more taxes when you file.

You could face penalties if you haven’t withheld enough throughout the year.

If your RSUs make up a significant part of your income, planning ahead helps you avoid a surprise tax bill.

How to Calculate RSU Taxable Income Yourself

To determine roughly how much of your RSUs will be taxable in a given year you can use this formula:

(# of Newly Vested RSUs) × (Market Value on Vest Date) = Taxable Income

Example Calculation of RSU Taxable Income

Let’s say you receive 1,000 RSUs that vest equally over four years.

After each vesting event, the fair market value of the stock on that day determines your taxable income.

In the example above, it’s pretty easy to calculate the taxable amounts since there’s only one batch of RSUs that’s vesting each year.

After the first year of vesting, many companies switch to monthly or quarterly vesting, which can make tracking taxable income throughout the year if you’re doing it manually.

If you want to skip the spreadsheets, your company will report the taxable income from your RSUs on your paycheck anytime you’ve had RSU income. This is often the easiest place to see the total taxable income, it just doesn’t tell you anything about the shares themselves.

RSU Taxes After Vesting: Capital Gains & Losses

As we’ve discussed, RSUs become fully taxable at vesting.

Once vested, your shares are now yours to hold or sell. But from this point forward, they’re subject to capital gains and loss rules, meaning you may owe additional taxes when you eventually sell.

How Cost Basis Affects Taxes

The stock price at the time of vesting typically becomes your cost basis per share. And will be the amount used to determine capital gains or losses when you sell.

Example:

Your RSUs vest when the stock price is $100 per share → Cost basis = $100 per share.

If you sell at $120, you have a $20 capital gain per share.

If you sell at $90, you have a $10 capital loss per share.

Capital Gains and Losses: How RSU Sales Are Taxed

When you sell your RSUs, you’ll either have a capital gain (if sold above your cost basis) or a capital loss (if sold below your cost basis).

If you sell at exactly your cost basis, there’s no gain or loss and no extra taxes are owed.

Short-Term vs. Long-Term Capital Gains and Losses

Capital gains from RSU sales fall into two categories: short-term and long-term. Which one applies depends on how long you hold your shares for after vesting.

If you hold for less than one year, your shares will be subject to short-term capital gains.

If you hold for longer than one year, your shares will be subject to long-term capital gains.

Here’s a table to help with the understanding:

As you can see from looking at the “Tax Treatment” column, the primary benefit of long-term capital gains is that their tax rates are less than short-term gains and ordinary income.

Holding RSUs for long-term capital gains isn’t necessarily a tax-saving strategy—it’s an investment decision. The real question isn’t “How do I save on taxes?” but rather, “Do I want to keep holding my company’s stock?”

Making a Plan for Your RSUs

Now that you have a better understanding of when and how you’ll be taxed on your RSUs, you’ll want to start making a plan to sell your RSUs.

There are many factors to consider when selling RSUs. It’s often recommended to sell RSUs immediately after vest if you’re able to.

Many financial professionals recommend that you treat your RSUs like a cash bonus and to sell everything that vests so that you can reinvest and use the cash elsewhere. While this can be an effective strategy, you’ll need to be sure that you actually reinvest the proceeds.

If you want to take on extra investment risk and leave some of your RSUs unsold, we recommend designating a percentage to keep from each vested batch and selling the remainder.

When Do I Owe Taxes on RSUs? – Final Thoughts

You don’t need to understand every tax detail, but knowing when RSUs are taxed, how much you might owe, and what happens when you sell will help you make smarter financial decisions.

Most people treat RSUs like a cash bonus—selling immediately at vesting to avoid concentration risk. But if you want to hold onto shares, setting a structured selling plan can help reduce risk while maintaining upside.

We published an article describing how much company stock is too much and to make your life easier, we built out an RSU Tax Calculator to help make estimating taxes a little bit easier.

Not sure what to do with your RSUs? We help clients optimize how they use their equity compensation through advice-only financial planning. If you’re interested, please schedule a call!