Avoid an ESPP Double Tax

Employee Stock Purchase Plans (ESPPs) rank high on our list of favorite employee benefits offered by tech companies. They can provide incredible upside with minimal upfront investment.

The only problem is that when you go to sell your ESPP shares, you can mistakenly end up overpaying on your taxes because of something called an “ESPP Double Tax.”

This ESPP Double Tax is a mistake that happens when you unintentionally pay both ordinary income tax and capital gains tax on the same portion of your sold shares.

Although it may not seem like a big deal, this mistake occurs frequently and can cost you tens of thousands of dollars unless you correct the error.

The purpose of this article is to discuss how the ESPP Double Tax issue happens, how to fix it, and go over a real example so you know exactly what to look for.

What Causes the ESPP Double Tax

There are 4 main reasons why people end up overpaying on their ESPP shares. (If you’ve read our article on the RSU double tax, you’ll notice similarities, but there are definitely key differences.)

Cause #1 of ESPP Double Tax - Cost Basis Will Vary

Cost basis refers to the amount you’ve invested as well as any amount you’ve already paid taxes on.

What’s nice about ESPPs is that you can easily look up how much you invested/contributed. What’s not-so-nice is that the taxes you pay when you sell ESPPs are complicated.

Assuming you sell your ESPP shares for gain, your gain will usually be composed of two portions that get taxed at different rates:

One portion will be taxed at ordinary income tax rates.

One portion will be taxed as capital gains.

The amount that gets taxed at each portion will vary based on:

The share price at the beginning of the ESPP offering period

The share price at purchase

The discount provided

The share price at sale

The time between purchase and sale

The portion that is taxed at ordinary income rates will show up on your pay statement.

The portion that is taxed as capital gains will show up on your investment account statements.

What matters here is that so long as you sell ESPP shares for a gain, there will almost always be a portion that’s subject to ordinary income taxes.

Cause #2 of ESPP Double Tax - Inaccurate Cost Basis Reporting

The biggest reason people end up overpaying on taxes with their ESPP shares is because the correct cost basis often does not get reported.

This shouldn’t happen, but due to the complexities of how the cost basis is determined upon the sale of ESPP shares, your cost basis is often misreported by your brokerage. This means that the ordinary income element also often goes unreported or underreported.

ESPP sales are considered “Covered Shares” which means that your brokerage will report transaction details to the IRS. However, just because they’re covered does not mean that the information they’re reporting is accurate!

Let’s look at a simple example of someone selling their ESPP Shares shortly after purchase:

The price at the beginning of your ESPP offering period was $80. (The actual length of the offering period will vary by company, but 6 months is pretty typical.)

The value of your company stock on the ESPP purchase was $100.

The actual price you paid for your ESPP shares was $68 a share.

And the price you paid when you ultimately sold your ESPP shares was $110. This means that you had a pre-tax gain of $42 a share or a 61.76% gain. Not too shabby!

Since you sold in an ESPP disqualifying disposition your taxable income will be:

$32 of Ordinary income per share ($100 - $68)

$10 of Short Term Capital Gains ($110 - $100)

You’re probably wondering what the problem is because this doesn’t seem too terribly difficult.

The issue is that your brokerage will often list your cost basis as the discounted price multiplied by the number of shares you purchased and will not take into account that the portion of ordinary income is being reported and paid through the employer.

Here’s what that looks like in another table:

In this example, for every share you purchased and sold, you’ll end up paying taxes twice on $32 of income per share if you don’t correct it.

So let’s say that you contributed $10k to the ESPP, you’d have purchased then sold 147 shares.

This error would have caused an extra $4,700 of short-term capital gains that shouldn’t have even been there. And depending on your tax rate, this could have caused you to pay an extra $1,700 in taxes.

Cause #3 of ESPP Double Tax - Tax Forms are Difficult

The next reason why this ESPP double tax issue happens so frequently is because tax forms are difficult to understand and sometimes they don’t even have data listed correctly.

Your paystub is where the ordinary income from ESPP sales shows up.

Your W-2 is where your employer shows all your income from the prior year. But sometimes your ESPP income just gets added to your total salary/compensation with no note identifying that that’s the case, which means there’s not an easy-to-read line item for your ESPP income.

Your brokerage will issue a 1099-B, but often the original 1099 is incorrect, so they’ll issue a supplemental 1099 with the correct details on it.

You’re not crazy for thinking tax forms are hard to understand. They are objectively difficult to understand and it’s not at all your fault.

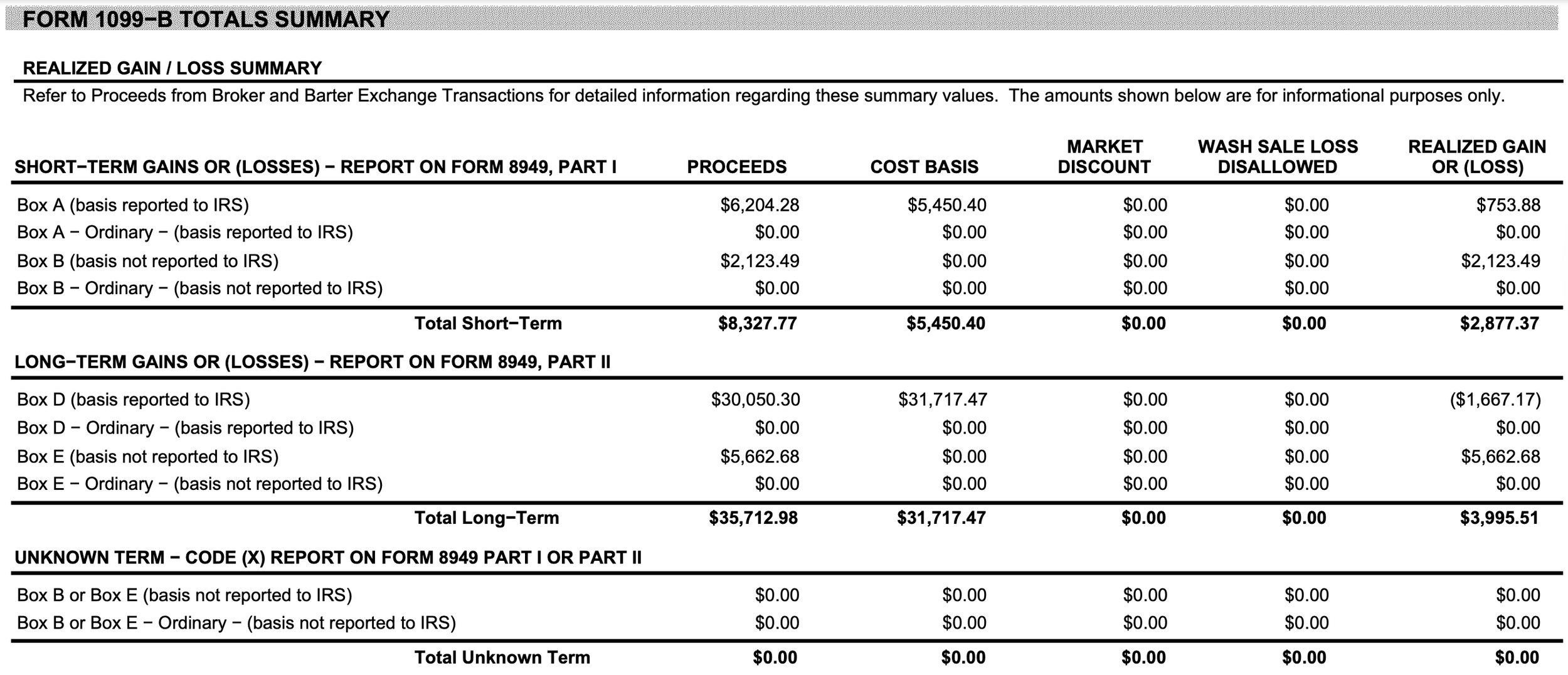

Here’s what an actual 1099-B looks like:

Sales of ESPP shares are categorized into two sale types, Short-term Covered and Long-term Covered. The “Covered” means that the cost basis was not reported to the IRS. It does not mean that the basis is accurate!

Here’s the section that shows the Short-term Covered transactions:

I’ll repeat: Just because a cost basis is listed and reported to the IRS, that does not mean that it is accurate

Cause #4 of ESPP Double Tax - Easy to Enter Incorrectly

The last cause/reason people pay tax twice on ESPP shares they’ve sold is because tax filing software makes it easy to miss.

If you’re not used to doing taxes, you probably feel little confidence that what you’re entering into TurboTax (or other) is actually correct.

Most tax prep programs ask you a series of questions to help you fill out your tax return. Eventually, there will be a question something like, “Do you have adjustments to this investment sale?”

If you aren’t aware of this common issue with ESPPs, it’s very easy to answer “No” to this question since “No” seems like a rational response. But you really should be answering “Yes” because you need to account for the income that’s already being accounted for!

How to Fix the ESPP Double Tax

If the basis on your ESPP shares is incorrect on your 1099-B, the best way to correct it is on your tax return itself. Before you can even do that, however, you have to be able to identify if the basis is wrong. And there is an easy method and a hard method.

Easy Method: Review Transactions Supplement

The easiest method to find and fix the ESPP double tax is to simply review your Transactions Supplement. (If you’re fortunate enough to have a company/brokerage that provides one.)

Companies and brokerages are aware of this double taxation issue with ESPPs so instead of only providing the standard 1099-B that could have errors, they provide what is basically a more detailed version of the 1099 that shows the transactions you had with the correct cost basis.

Here’s a sample Transactions Supplement that was provided in addition to the 1099-Bs we saw earlier in this article.

This sample includes both RSU sales and ESPP sales, but if you look closely at the column “Adjusted Gain (Loss)” you can see that there are adjustments to be made to both the RSUs and the ESPP shares.

So the easiest way to find and fix your ESPP double tax issue is to simply review this document and make corrections in your tax prep software.

Hard Method: Review the 1099-B, Sale Confirmations, Paystub, and W-2

If your company does not issue a Transactions Supplement, unfortunately, you’re going to have to put on your detective hat and do some digging.

Here’s the list of the documents you’ll want to gather:

Year-end paystub

W-2

1099-B

Purchase confirmations for all the ESPP shares sold

The quickest way to figure out if something fishy is going on is to look at your 1099-B and figure out how the 1099-B is calculating the cost basis on your ESPP sales.

From our example earlier, the 1099-B showed that there was a 3/17/2023 sale of 17.5169 shares of stock that had been purchased on 6/30/2022 with a cost basis of $5,450.40.

Once you’ve identified the transaction you want to investigate, the next step is to take the total cost basis and divide it by the total number of shares purchased. This gets us a share price of $311.151.

If this share price is identical or nearly identical to the discounted stock price you paid on 6/30/2022, you know that the reported cost basis on the 1099-B is probably not including the income that showed up on your paystub when you sold these shares.

To further investigate, you’ll want to look at the purchase confirmation of the sold shares to see how similar the price is. If it is the same, then you’re at risk of overpaying taxes. (Or you may have already overpaid.)

You can then check your year-end paystub (or the paystub that was generated immediately after your ESPP sale) and you will see a line item that shows income from ESPP shares sold.

Example of Someone with an ESPP Double Tax

Whether you noticed it yet or not, the example we’ve been looking at is an example of this ESPP double tax in action. If you look back at the adjusted 1099-B, you can see that there was $1,873 of missing cost basis from the ESPP shares that were sold.

Depending on your tax bracket, that $1,873 of missing cost basis could cost you up to $900 of tax overpayments!

The damage in the example we shared is pretty mild compared to others we’ve seen.

By preventing or correcting this common error, we’ve helped clients avoid thousands of dollars of extra taxation.

ESPP Double Tax Conclusion

If you sold ESPP shares in the prior tax year, you’ll want to double-check that everything is in order on your tax return. If you’ve sold ESPP shares for large gains, just be aware that the larger the gains, the larger the overpayment in taxes could be paid.

Taking 15 minutes to review old statements and tax forms could save you tens of thousands of dollars.

We’re here to help you uncover potential tax errors and reclaim your overpaid taxes. Learn more about our PlanFTW service here.

If you happen to work at Remitly, we’re offering a group discount on our PlanFTW engagement. (Please note that we have caught this ESPP Double Tax issue for other Remitly employees so this very likely applies to you.)

If you want to go it alone, we’ve built out a calculator that can help you guesstimate what your cost basis should be and we’d be happy to share it with you.

Thank you for reading and please reach out to team@equityftw.com if you have any questions.